|

| Retail Burn |

|

|

|

|

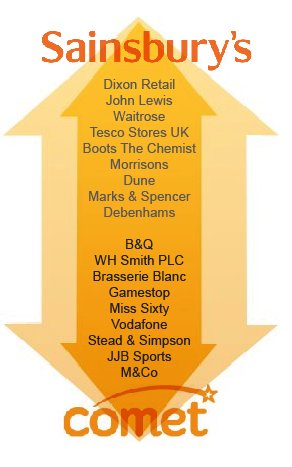

| This month, the most talked about retailers, according to SnapShop and the Retail Burn, include Sainsbury's,

Dixon Retail,

John Lewis,

Waitrose ,

Tesco Stores UK,

Boots The Chemist,

Morrisons,

Dune,

Marks & Spencers ,

Debenhams,

B&Q ,

WH Smith PLC,

Brasserie Blanc,

Gamestop,

Miss Sixty,

Vodafone,

Stead & Simpson,

JJB Sports,

M&Co and

Comet.

The retailer with the highest number of positive news articles in November was Sainsbury's, with reports that the supermarket is to recruit an extra 5,000 seasonal workers to meet increased demand from customers.

At the other end of the scale, Comet with speculation that the retailer is unlikely to be trading beyond Christmas.

|

|

|

|

|

|

|

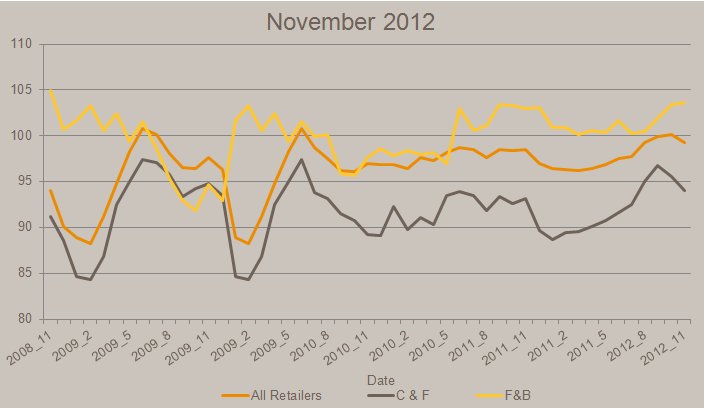

| The FSP Retail News Index is a 3 month moving average measure of sentiment in reported retail news stories.

The November RNI index for All Retailers dropped (for the first time since May 2012) to 99.

Household and Clothing & Footwear also dropped this month. Household saw a significant drop, from 99 to 93.

Grocery, Personal, Food & Beverage and Leisure all went up in November.

For the full report, click here.

FSP on average reviews over 350 unique items of retailer news. Each article is scored according to sentiment. RNI is the sum of these scores indexed against 2005 and averaged over a three month period. The RNI time series for all retailers starts from May 2002. |

|

|

| Product Focus |

|

|

|

Cost-effective Research for Out-of-Town Assets

Out-of-Town (OOT) retailing accounts for around 30% of comparison shopping expenditure. With figures from CBRE showing that OOT accounts for about 60% of the retail development pipeline, that share is set to grow.

A critical challenge for the effective management of OOT retail assets is to identify relevant potential occupiers for whom a solid business case for taking new space can be developed. The accurate specification of potential target occupiers depends in turn on identifying the number and profile of consumers who will be attracted to the location.

When economic conditions were easier, the level of evidence required for taking a new outlet was lower than in these more challenging times. The penalties for making a marginally sub-optimal decision have increased.

To address this increased need for accurate and comprehensive information, FSP has developed a new, tailored service for OOT asset managers. Readily accessible data about every retail and leisure park in the U.K. is now available on an in-house database for analysis and comparison. The information covers both potential shoppers and the current occupiers for each park.

The number and profile of potential shoppers at any park can be compared with those at other parks of the same type. For asset managers considering the acquisition of an additional park, the fit with the existing portfolio can quickly be established. When making the case to an occupier to take a new unit, its potential can be set within the context of the potential within the occupier’s existing portfolio.

The new database has been developed in response to FSP client requirements and has already demonstrated its effectiveness. If you have an asset that you think might also benefit, please get in touch.

|

|

|

|

|

|

|

|